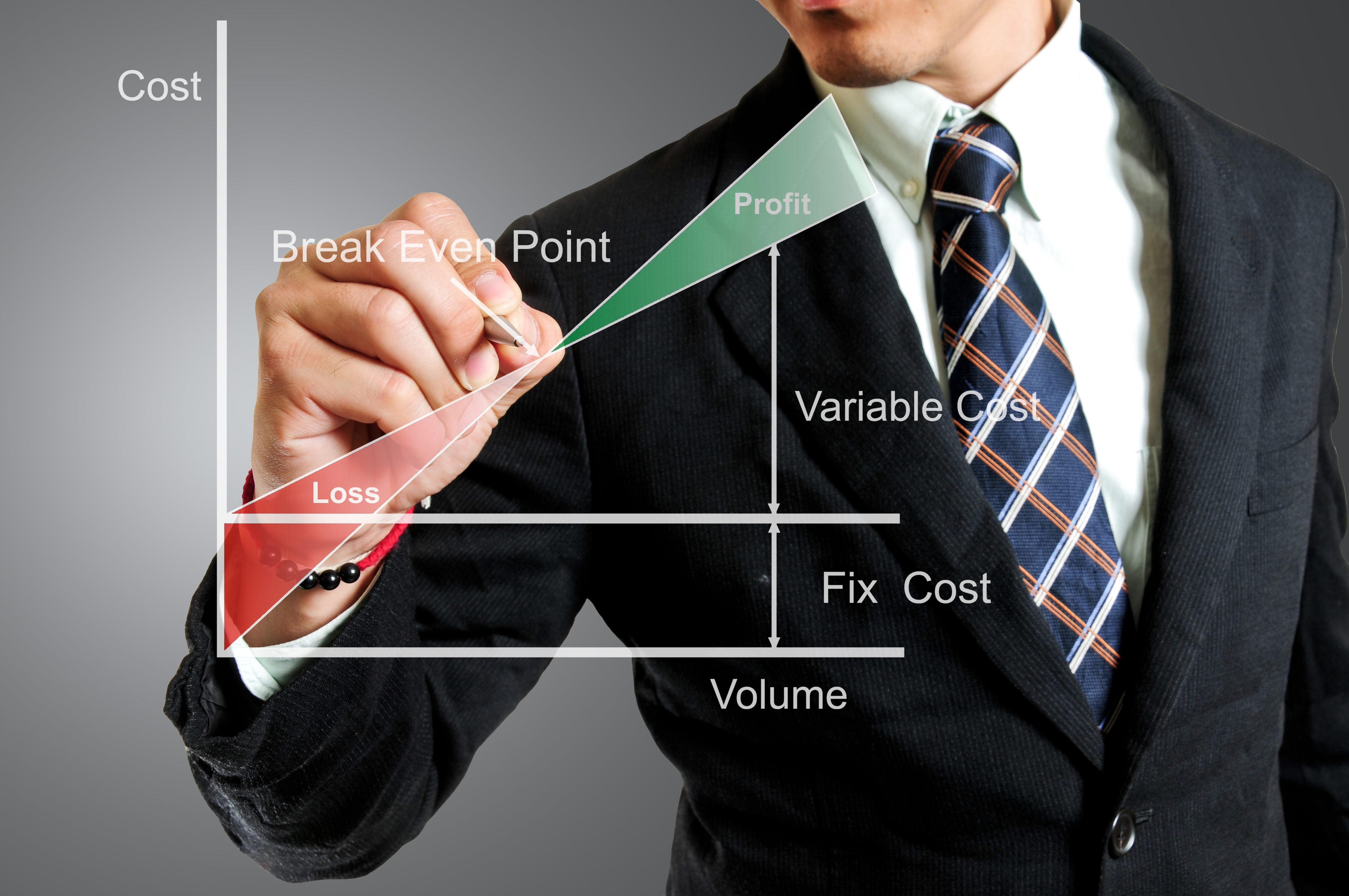

5 Accounting Equation Rules Suited For Sole Proprietorships

Accounting procedures for sole proprietorships contain certain differences compared to accounting catered to other corporations. Most corporate accounting services in Singapore are well versed enough to conduct accounting procedures for sole proprietorships. However, as a method of safeguarding and minimising potential errors, business owners are encouraged to remember these 5 accounting equation rules:

- Basic

The basic accounting equation for sole proprietorships are calculated with Assets being a sum of Liabilities as well as the Owner’s Equity (Assets = Owner’s Equity + Liabilities). Business transactions for sole proprietorships are recorded into specific accounts that are contained in the corporation’s general ledger. Some of the accounts that users have to pay attention to would be the Temp service expense account, Advertising account, Service revenues, Notes payable, Accounts Payable, Equipment purchase, Accounts receivable, Cash, the Owner’s Equity account and Contra Owner’s Equity account.

- Draws

Draws are termed for withdrawal of corporate assets by the owner of the sole proprietorship for personal use. These withdrawal of assets are not considered expenses, and therefore the transactions are not typically reported in the income statements. In the event that withdrawals were made, the accounting equation of the sole proprietorship would reflect the decrease in both assets as well as owner’s equity, thereby making the equation in balance.

- Loans

Another factor that affects the accounting equation would be loans from banks. Should the business owner borrow currency, there will be an increase in the sole proprietorship’s assets as well as liabilities. This transaction should be recorded in both the Cash section of the asset account, as well as Notes Payable in the liability account. Do take note that the bank loan is not considered as earned revenue, therefore there will be no effect from this transaction in the income statement. One can however, interpret two sources for the sole proprietorship assets- the owner of the company’s provisions, as well as the creditors (bank).

- Earned Revenue

As per standard billing procedures where payment due dates are usually after 30 days, the revenue transaction is not recorded into the capital account just yet despite the fact that both assets and owner’s equity displays an increase based on the payment amount. The amount earned should be recorded under the Service revenues section of the revenue account so that the revenues can be reported into the income statement at any given time and transferred to the owner’s capital account after the year end.

- Missing Amount

In the event that there are missing amounts, the accountant may rely on the statement of changes recorded in the owner’s equity to determine the components that are unknown. For example, relying on the draw amount at the beginning as well as end balances of the owner’s equity to calculate and derive the net income value.